FINANCIAL HIGHLIGHTS

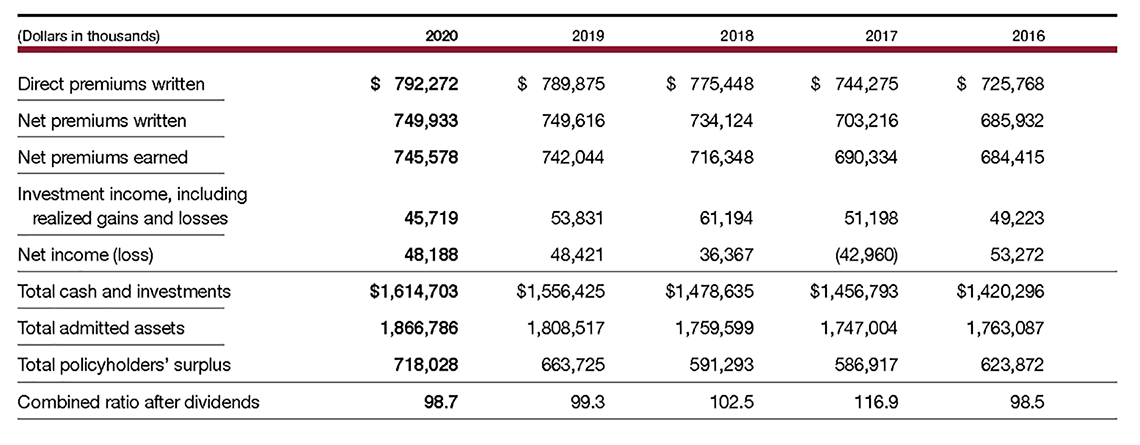

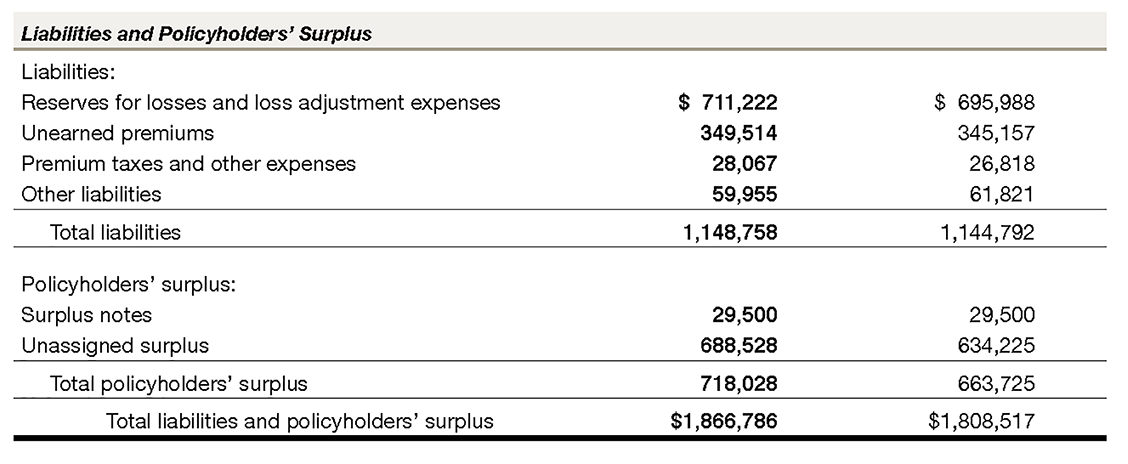

The combined financial performance of Penn National Insurance for the year ended December 31, 2020, produced net income of $48.2 million. This enabled our company to add $54.3 million to its policyholders’ surplus since December 31, 2019, to a total of $718.0 million.

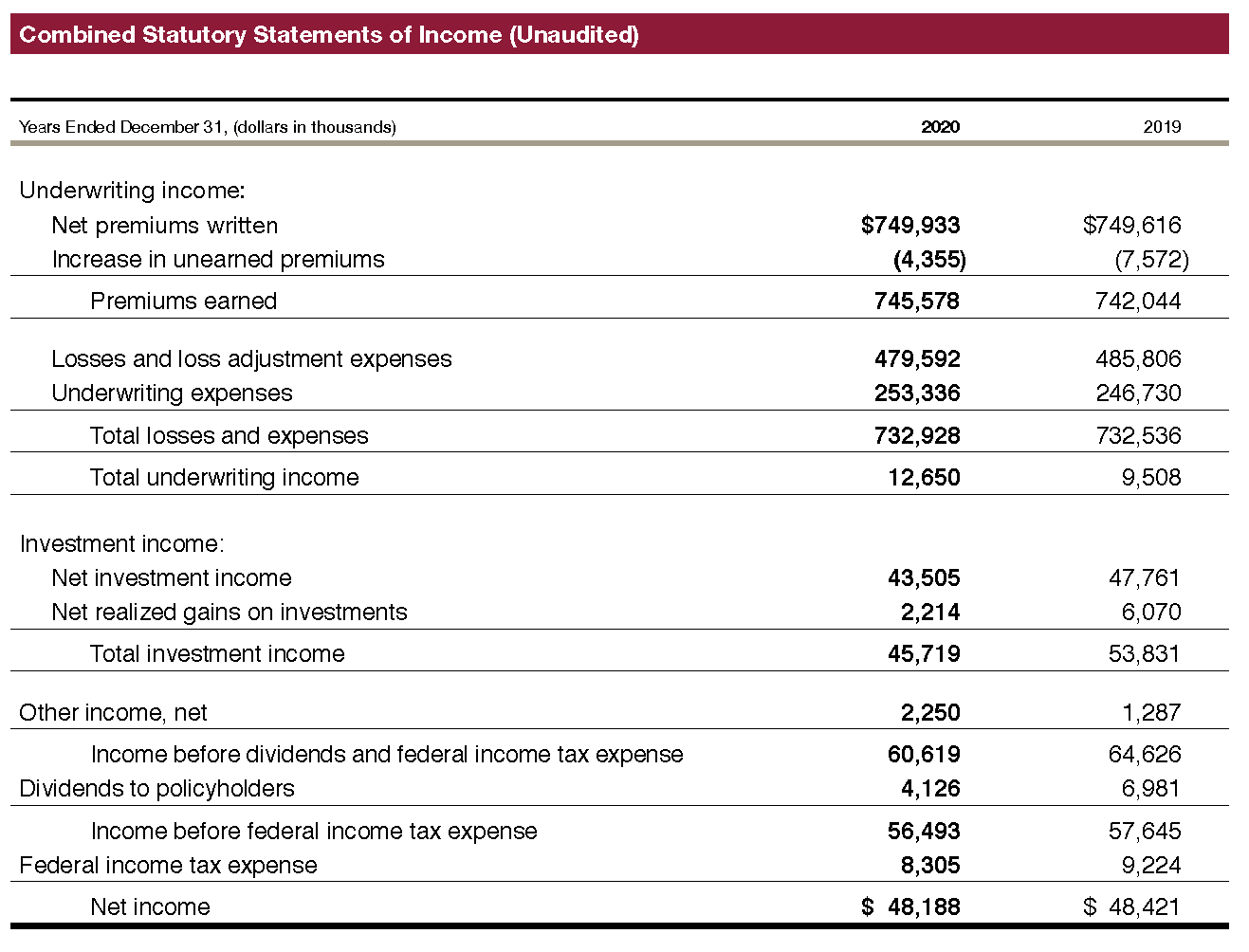

Total net premiums written and earned of $749.9 million and $745.6 million, respectively, were up slightly from the prior year. As rate firming continued to favorably impact renewal pricing, direct premiums written for our commercial lines were up by $12.9 million or 2.9 percent from last year, reaching $451.4 million for the year ended December 31, 2020. Personal lines direct premiums written of $340.9 million were less than the prior year by $10.5 million or 3.0 percent. This decrease was partly caused by $5.7 million in personal automobile refunds given to policyholders in the wake of the COVID-19 pandemic.

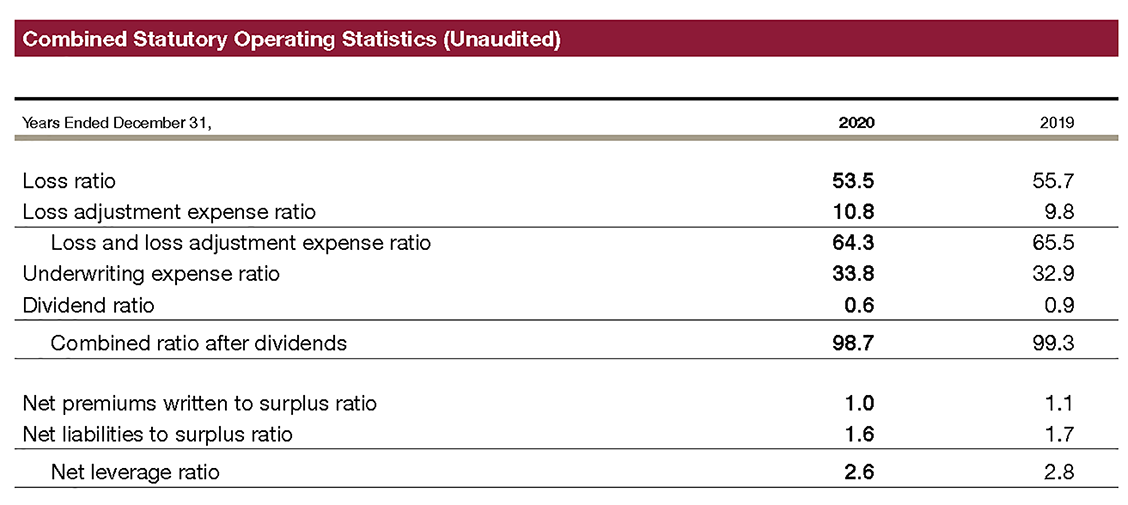

Overall, incurred losses and loss adjustment expenses totaling $479.6 million during 2020 were $6.2 million less than those incurred during 2019. Non-catastrophe losses were less than the previous year, primarily driven by both the commercial and personal automobile lines of business. Catastrophe losses, however, were significantly higher than our company’s normal experience level, as seen in the homeowners, businessowners and fire lines. Including net unfavorable development of $1.7 million, total net catastrophe losses and LAE incurred were $55.9 million or 7.5 points for the year ended December 31, 2020, compared to $25.1 million or 3.4 points for the prior year. Our 2020 net loss and loss adjustment expense ratio was 64.3, an improvement of 1.2 points from the 2019 ratio of 65.5.

Underwriting expenses for the year ended December 31, 2020, increased by $6.6 million from the prior year. This was largely driven by higher commission costs. There was no commission reduction relating to the 2020 COVID-19 policyholder premium refunds, and contingent commissions were greater due to favorable loss experience for the year.

Our reported net combined ratio for the year came in at 98.7, which was 0.6 point better than the 2019 combined ratio. This improvement was primarily attributable to the 1.2 point decrease in the loss and loss adjustment ratio. The dividend ratio also improved compared to the prior year, by 0.3 point, while our underwriting expense ratio increased by 0.9 point. Total admitted assets rose $58.3 million from December 31, 2019, to $1.9 billion as of December 31, 2020.

Click to download 2020 Combined Statutory Financial Statements